GBL, a prominent Belgian holding company, has its roots intertwined with the Société Générale de Belgique.

The Democratic Republic of the Congo (DRC), formerly known as the Belgian Congo, has valuable mineral resources. Copper, cobalt, uranium, gold, and diamonds that have fueled western development for over a century. Yet, the Congolese people remain among the most impoverished in the world.

At the heart of this paradox lies two entities: Union Minière du Haut-Katanga (UMHK) —the colonial-era mining giant—and its parent company, Société Générale de Belgique , whose legacy persists today through their successors, Groupe Bruxelles Lambert (GBL) and Suez. They both have a market capitalization of over USD$50billion, and over 200billion in annual revenues.

These companies have amassed billions while leaving Congo impoverished. They have no single mine on Belgian territory. Where does all this wealth come from?

The Birth of UMHK: A Colonial Enterprise

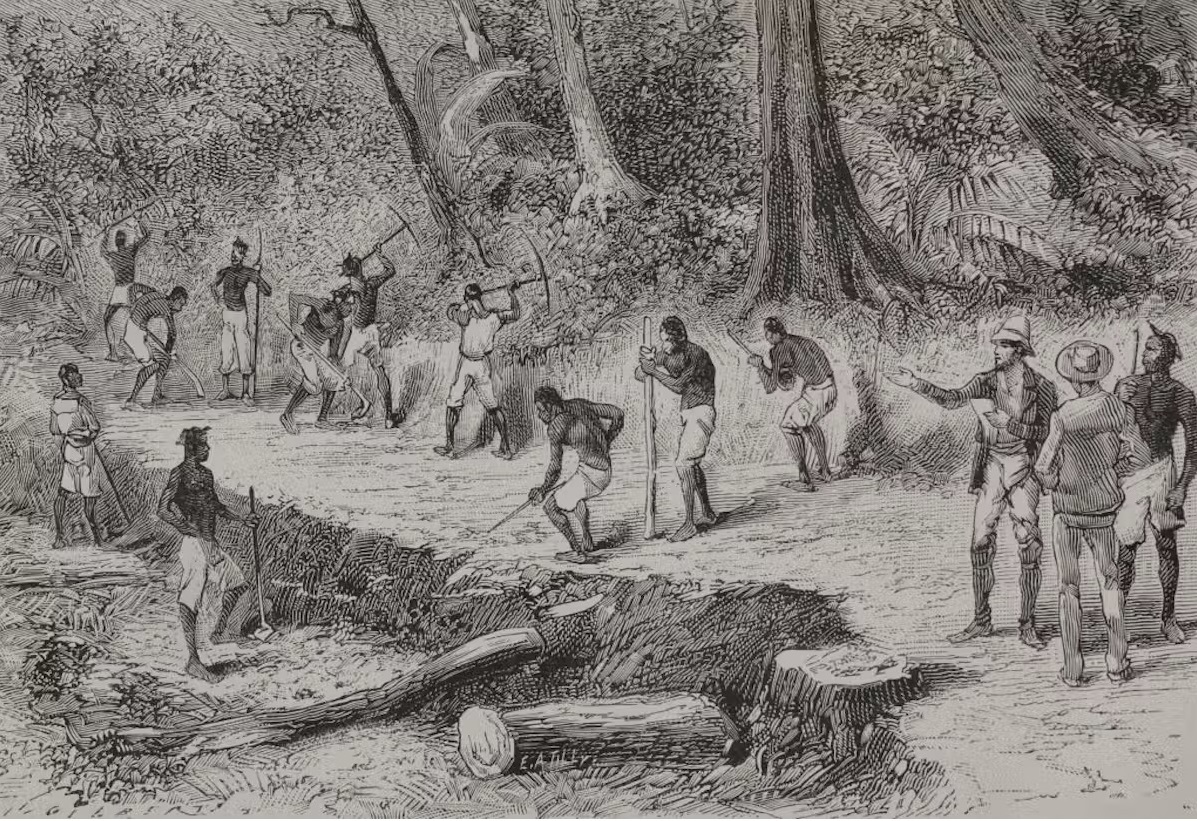

In 1906, Société Générale de Belgique, one of Belgium’s largest industrial conglomerates, founded Union Minière du Haut-Katanga (UMHK) to exploit the mineral-rich Katanga region in south-eastern Congo.

The Belgian state had already established itself as the colonial ruler of Congo under King Leopold II, who treated the territory as his personal fiefdom until public outcry forced him to transfer control to the Belgian government in 1908.

Under colonial rule, Congo became a source of raw materials for Europe’s burgeoning industrial economy, with UMHK at the center of this extractive enterprise.

UMHK quickly became one of the most profitable mining companies in the world. By the 1950s, it accounted for 7% of global copper production and 60% of cobalt production, generating annual revenues equivalent to $2–3 billion in today’s dollars.

Its operations were vast, employing tens of thousands of Congolese workers subjected to brutal conditions, including forced labor, low wages, and systemic abuse. Meanwhile, profits flowed back to Belgium, enriching Société Générale de Belgique and the Belgian monarch.

One of UMHK’s most infamous contributions came during World War II, when its Shinkolobwe mine supplied high-grade uranium ore to the United States for the Manhattan Project. This uranium was used to develop the atomic bombs dropped on Hiroshima and Nagasaki—a stark reminder of how Congo’s resources shaped global history without benefiting its people.

Katanga Secession Crisis: Belgium’s Hidden Hand

When Congo gained independence in 1960, tensions erupted between the central government in Kinshasa and regional leaders seeking autonomy or secession. None was more contentious than the attempted secession of Katanga, led by Moïse Tshombe and supported by foreign powers, led by Belgium.

Katanga’s mineral wealth made it strategically vital, and UMHK played a pivotal role in financing and sustaining the rebellion.

Belgium covertly backed the Katangan separatists, deploying approximately 10,000 troops under the guise of “protecting European lives” but actually aiming to safeguard UMHK’s interests. These forces trained and armed Katangan militias, enabling them to resist efforts by the newly independent Congolese government to assert control over the province.

The Katanga crisis exemplifies how Belgium manipulated post-independence politics to maintain access to Congo’s minerals. Even after the secession failed in 1963, Belgium continued to exert influence over Congo’s mining sector until UMHK was nationalized in 1966 and absorbed into Gécamines, the state-owned mining company.

From Nationalization to Privatization: The Evolution of UMHK

After nationalization, UMHK ceased to exist as an independent entity, but its assets and infrastructure formed the foundation of Gécamines. However, mismanagement, corruption, and declining investment plagued Gécamines throughout the Mobutu era (1965–1997). By the late 1990s, Congo’s mining sector was in shambles due to decades of neglect and civil war.

A road being built in the Belgian Free State in 1890. PHAS/Universal Images Group/Getty Images

Enter the era of privatization. In the early 2000s, under pressure from international financial institutions like the IMF and World Bank, Congo began selling off its mining concessions to multinational corporations.

Companies like Glencore, Freeport-McMoRan, and others acquired stakes in former UMHK sites, reviving Congo’s position as a global leader in copper and cobalt production.

Today, Glencore dominates Congo’s mining landscape, generating billions in revenue annually. In 2022 alone, Glencore reported total revenues of approximately $200 billion, with a significant portion coming from its Congolese operations.

Despite this, Congo’s share of the profits remains minimal, perpetuating the cycle of exploitation that began under colonial rule.

The Legacy of Société Générale de Belgique

While UMHK no longer exists, its parent company, Société Générale de Belgique, underwent significant transformations in the latter half of the 20th century. Facing economic pressures and changing market dynamics, it split into two main successor entities today:

- Groupe Bruxelles Lambert (GBL):

- GBL has ploughed its big mineral profits into global corporations across various sectors, including Imerys, Pernod Ricard, and Adyen.

- As of 2023, GBL has a market capitalization of approximately €20–25 billion ($22–28 billion).

- Although Belgium does not have any mines, GBL combined revenues exceed €100 billion annually.

- Suez:

- Publicly, Suez is involved in water management, waste treatment, and energy services, originating from Société Générale de Belgique’s utilities division.

- As of 2023, Suez has a market capitalization of approximately €10–15 billion ($11–17 billion) and reported revenues of around €17–18 billion ($19–20 billion) in 2022.

These companies bear little resemblance to their colonial predecessors, yet their existence is deeply rooted in the exploitation of Congo’s minerals. Today, neither GBL nor Suez owns any mines in Belgium, and their logos don’t appear anywhere in Congo, but their existence underscores the enduring impact of colonialism on Congo’s resource curse.

Modern-Day Exploitation

In 1988, the French conglomerate Suez acquired the Société Générale de Belgique. This acquisition marked a significant shift in the control of Belgian industry and finance, as the Société Générale de Belgique had been a dominant force in these sectors.

Despite changes in ownership and governance, Congo’s mineral wealth continues to be extracted primarily for the benefit of European and American companies, and governments. The rise of electric vehicles has driven unprecedented demand for cobalt, much of which comes from Congo.

Multinational corporations like Glencore dominate the supply chain, often accused of perpetuating exploitative practices, environmental destruction, and human rights abuses.

Artisanal mining—a small-scale, informal sector involving millions of Congolese workers—is another dark chapter in this story. Child labor, unsafe working conditions, and toxic exposure are rampant, yet international companies sourcing minerals from Congo rarely address these issues adequately.

The history of UMHK, Société Générale de Belgique, and their successors reveals a pattern of exploitation spanning over a century. From colonial-era extraction to modern-day multinational dominance, Congo’s mineral wealth has fueled global industries while leaving the country mired in poverty and conflict.

Today, Groupe Bruxelles Lambert (GBL) and Suez are worth billions. Their success is built on a foundation of colonial plunder and ongoing inequality. For Congo, the promise of prosperity remains elusive, trapped in a cycle of exploitation that shows no signs of ending.

Links to current government of DRC

The deep-rooted ties between Groupe Bruxelles Lambert (GBL) , Suez , and the Belgian state reveal why these entities have historically maintained a vested interest in controlling or influencing governance in Congo. Congo’s mineral wealth has been integral to Belgium’s economic prosperity since the colonial era, and losing access to this resource would destabilize not only the financial standing of companies like GBL and Suez but also the broader Belgian economy.

For decades, UMHK’s operations provided the raw materials that fueled industrialization and technological advancement in Europe, while Société Générale de Belgique reaped immense profits as its parent company. Even though GBL and Suez no longer directly control mines in Congo, their portfolios are indirectly tied to global industries—such as energy, manufacturing, and technology—that depend on Congolese minerals.

A stable, pro-Belgian government in Congo ensures uninterrupted access to these critical resources, which remain foundational to modern economies. Without this access, Belgium risks undermining its industrial base and sliding into economic irrelevance—a scenario akin to being pushed “into the stone age.”

Moreover, the influence wielded by GBL and Suez extends beyond mere economics; it is deeply political. These companies, through their historical connections to the Belgian state, have long acted as proxies for national interests in Congo.

By maintaining leverage over Congolese governments—whether through diplomatic pressure, corporate lobbying, or covert manipulation—they safeguard Belgium’s strategic foothold in one of the world’s most resource-rich regions.

Should an independent or nationalist Congolese government emerge, prioritizing local development over foreign exploitation, it could nationalize assets, impose stricter regulations, or redirect profits away from Western corporations. Such a shift would cut off the lifeblood of companies like GBL and Suez, whose legacies and current valuations are intrinsically linked to Congo’s minerals.

Thus, ensuring favorable governance in Congo is not just about preserving profit margins—it is about securing Belgium’s continued relevance in a global economy increasingly driven by rare earth elements and green energy technologies sourced from Congo. Letting go of this control would mean relinquishing a lifeline that has sustained Belgium for over a century.

This is the story of Belgian companies worth billions—with no mines.